Third EU Hydrogen Bank Auction Results: What Baltic PtX Players Should Take Away

The third European Hydrogen Bank auction closed at €1.09 billion across nine winners and surfaced clear signals for any developer eyeing Baltic green hydrogen and PtX projects. Here is what the bid prices, basket dynamics and AaaS moves mean for how Baltic PtX ecosystem stakeholders should shape the next round.

NEWS

PtXBaltic

5/8/20264 min read

Third EU Hydrogen Bank Auction: Reading the Signals for the Baltic PtX Ecosystem

Brussels announced the IF25 results on 7 May. Nine winners, €1.09 billion, 1.1 GW of electrolyser capacity — and a set of dynamics that Baltic PtX ecosystem stakeholders should study now, not when the next call opens.

The European Hydrogen Bank's third round closed with nine projects awarded across three baskets, totalling €1.09 billion in fixed-premium support and roughly 1.3 million tonnes of RFNBO and low-carbon electrolytic hydrogen over a 10-year payout window. Winning bids landed between €0.44/kg and €3.49/kg. Greece and Austria appeared on the winners' list for the first time. Finland took the largest single award. Norway swept the maritime-aviation basket. CINEA expects to sign grant agreements in Q4 2026, with financial close required within 2.5 years and start of operations within 5 years of signature.

Competition is tightening, and the price ceiling is dropping

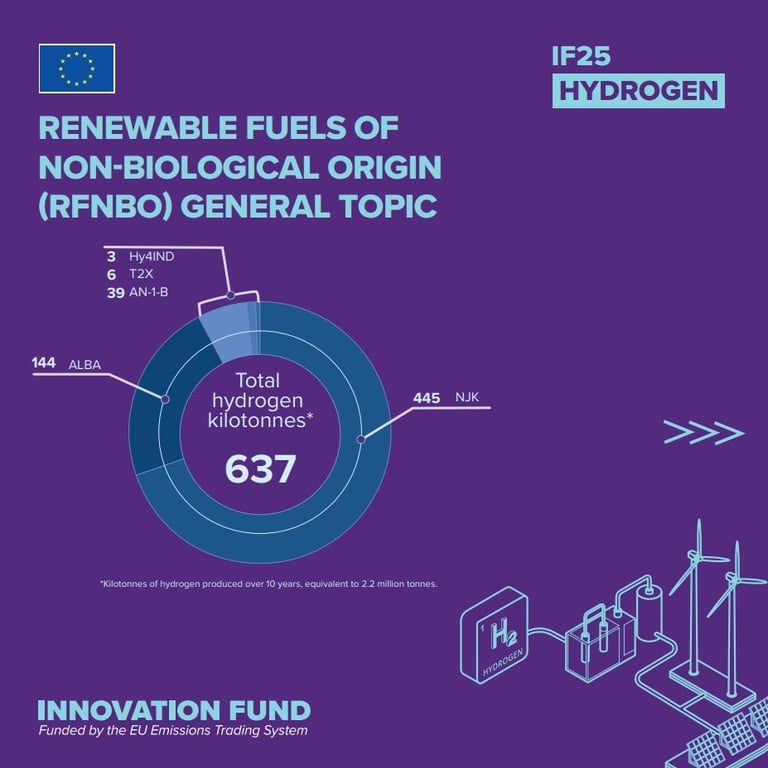

Basket 1 — RFNBO production with no end-use restriction — pulled 50 bids requesting €7.3 billion against a €600 million pot. That is a 7× oversubscription, and the five winners cleared at €0.57–€0.98/kg. For context, the second auction's general topic awarded between €0.20 and €0.60/kg; the bid window has crept up modestly but the overall message stands: developers are willing to clear at well under €1/kg for general-purpose RFNBO. The premium that wins is not the premium most Baltic project economics are sized around. If a project's CAPEX, RES PPA price and electrolyser load factor cannot get to a sub-€1/kg fixed premium and still close the bankability gap, the general basket is no longer the right door — at least not without rethinking offtake structure or stacking national support.

The maritime-aviation basket is the structurally different game

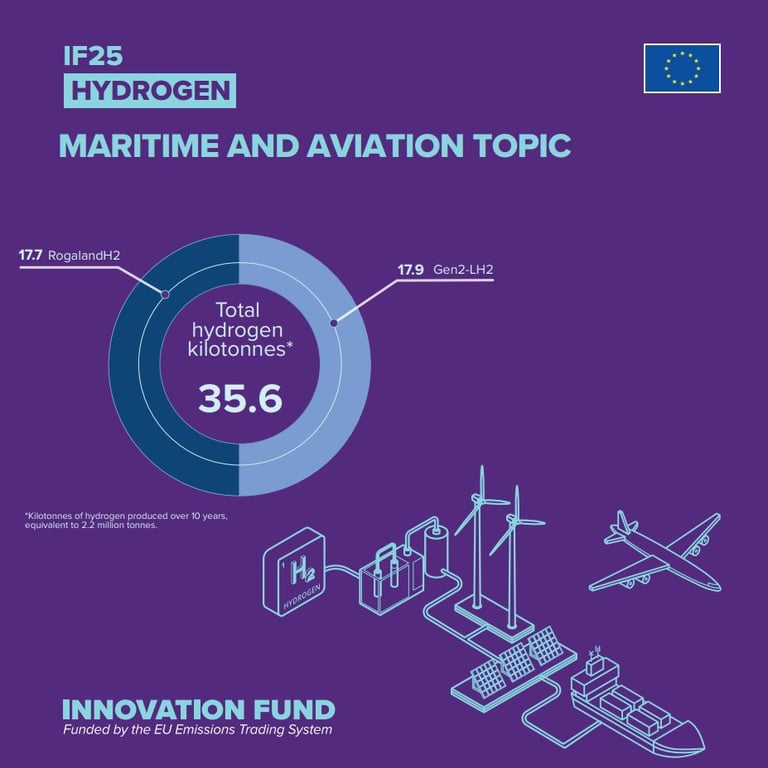

Basket 3 received only 3 bids against a €261 million budget and was undersubscribed by €137 million. The two Norwegian winners cleared at €3.48 and €3.49/kg — almost a different planet from the general basket. The reason is not generosity; it is that maritime and aviation offtakers pay a much higher counterfactual price for fossil molecules, the project sizes are smaller, and the certification-plus-offtake complexity narrows the bidder field. For Baltic PtX ecosystem stakeholders looking at port-based green ammonia, e-methanol or aviation SAF feedstock — the precise corridor that ports like Ventspils, Liepāja, Klaipėda, Tallinn and Muuga are quietly working on — this is the basket where Baltic geography genuinely competes. Undersubscription is a direct invitation: if your project has a credible maritime or aviation offtake, the next call is the most navigable route to grant funding the EHB has yet offered.

Auctions-as-a-Service is becoming a parallel funding architecture

The headline €1.09 billion is no longer the whole story. Three Spanish projects will sign under Spain's national €304 million RFNBO budget plus €136 million for maritime/aviation offtake. Three Danish projects will sign under Germany's €1.3 billion AaaS pot, dedicated to RFNBO production tied to the Danish-German hydrogen interconnector with offtakers on the German side. That last detail matters more than it looks. RED III transport quotas are now transposed in Germany, the demand pull is concrete, and Berlin is willing to put national money behind cross-border supply that lands in German offtaker hands. Lithuania already participated as an AaaS host in the second round; Spain and Austria did the same. Latvia and Estonia have not. The mechanism is open, the precedent is established, and the strategic question for Baltic capitals is whether to remain auction takers or to use AaaS to channel national funding toward locally-rooted projects on a level legal footing with the EU pot.

What the winning bids quietly reveal about project design

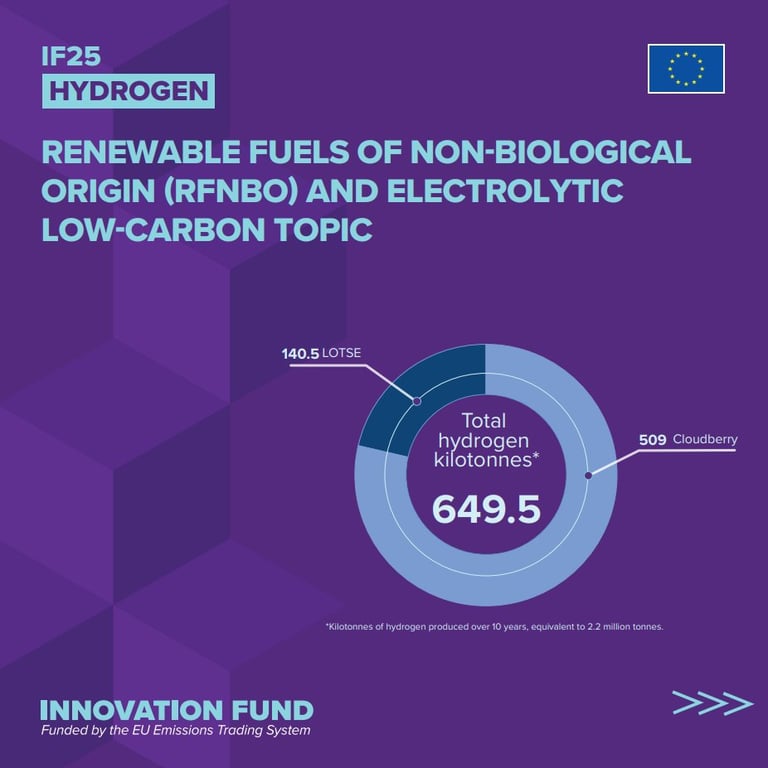

Vetyalfa's 500 MW Cloudberry project in Vaaka, Finland cleared at €0.44/kg under Basket 2 — the lowest premium of the entire round and the largest single project. Copenhagen Infrastructure Partners' 120 MW Lotse project in Germany cleared at €1.10/kg in the same basket. Hellenic Hydrogen's 100 MW Greek project, Wiener Stadtwerke's 5 MW Austrian Hy4IND, two Danish wins and one Spanish win filled out Basket 1. Patterns worth noting: the cheapest bids came from large-scale projects with strong RES build-out (Nordic wind), tight coupling between production and transport-sector offtake mandated by RED III, and developers with prior auction experience. Small projects can still win — the 5 MW Austrian project proves it — but only with a clearly differentiated offtake story or a regulated host-country market that supports the price stack. Baltic projects that fall in the 20–100 MW range need to make the offtake math defensible before bid day, not after.

Practical takeaways for Baltic PtX ecosystem stakeholders

The next IF call is not yet announced, but the windows tend to open in late autumn for a winter close. That gives the Baltic PtX ecosystem stakeholders roughly six months to act on the lessons of round three rather than rediscover them under deadline pressure. The honest priorities:

Look hard at the maritime-aviation basket — it is undersubscribed, the price ceiling is genuinely high, and the Baltic Sea ports network is one of the more credible regional fits in the EU. Tighten offtake before tightening CAPEX — a binding or near-binding offtake LOI with a German, Polish or Nordic counterparty changes the bid stack more than another round of EPC optimisation will. Engage Latvia's and Estonia's energy ministries on AaaS — the mechanism is becoming the parallel rail, and not having a national hosting pot leaves locally-rooted projects competing only on the EU pot's tighter terms. Stack funding deliberately — CEF feasibility funding, Innovation Fund regular calls, REPowerEU windows, the Hydrogen Bank, BEMIP, and bilateral Danish-German pipeline-linked support are not interchangeable; they are sequenced. Build the bid file in summer, not in February — the winners are not the projects that wrote the best application; they are the projects that had the cleanest bankability story when the call opened.

Closing read

Three rounds in, the Hydrogen Bank has stopped being a pilot and started being a standing market mechanism. The bid prices are converging, the AaaS pots are growing, the maritime-aviation door is open, and RED III transport is shifting demand from aspirational to contractual. Baltic projects have the geography, the RES potential and — increasingly — the corridor infrastructure to play seriously. What is missing in most cases is not engineering or ambition; it is a value proposition that maps cleanly onto the auction's pricing logic and the right basket. The teams that translate the May 7 results into a sharper bid file between now and the next call are the teams that will be in the next winners' list.

Source: EU awards over €1 billion to European hydrogen projects to accelerate the clean transition